Mutual fund portfolio mastery: how smart investors build, review and improve their funds

Owning 15 funds doesn't mean you have a portfolio — it means you have a mess. Learn how to build, review and improve your mutual fund portfolio using asset allocation, rolling returns, Sortino ratio & active weight analysis. From random SIPs to a real investment strategy.

Mutual fund portfolio mastery: how smart investors build, review and improve their funds

CashFlowCrew.in|Mutual fund education

Most investors hold mutual funds but very few manage them like a real portfolio. 65% of US large-cap mutual funds underperformed the S&P 500 in 2024 — which means simply buying popular funds is not enough. What shapes your outcome is not one "star" fund, but how all your funds work together as a single coordinated portfolio.

Key takeaways

At a glance

Question | Answer |

|---|---|

What is a mutual fund portfolio? | The combination of all mutual funds you hold across goals, accounts, and platforms — managed as one coordinated strategy, not isolated funds bought at random times. |

How often should I review it? | Every 6 to 12 months — focusing on performance, risk-adjusted returns, asset allocation, and costs. Not every market movement. |

Can I rely only on SIPs and ignore strategy? | No. SIPs build discipline but without asset allocation, risk control, and periodic review, even good SIPs can lead to a poorly constructed portfolio. |

What advanced techniques matter? | Rolling returns, Sortino ratio, alpha and beta, and active weight calculations — these move you from guesswork to data-driven portfolio analysis. |

Is this investment advice? | No. Education only. Consult a SEBI-registered RIA for personalised advice. |

Section 1

What is a mutual fund portfolio and why it matters more than individual funds

When we look at investors' accounts, we often find 10 to 20 funds with overlapping holdings, unmanaged risk, and no clear goal mapping. The goal is to move from a random collection of funds to a structured portfolio that supports your goals with clarity and purpose.

View your funds across all platforms as one integrated portfolio

Define clear goals and timelines for each part of the portfolio

Focus on overall portfolio risk — not just individual fund performance in isolation

Section 2

Core building blocks: asset allocation and SIP investment strategies

Before worrying about which specific scheme to buy, decide how much of your portfolio goes into equity, debt, and hybrid categories. This asset allocation decision typically drives a larger part of your long-term result than picking one fund over another.

SIP investment is a powerful tool — but SIPs must fit into a plan. An aggressive equity SIP for a goal 3 years away creates unnecessary volatility. A conservative debt-heavy SIP for a 20-year retirement goal may be too slow to grow. Match the risk level to the timeline.

Key asset allocation questions

What portion of your portfolio should be in equity based on your risk profile and time horizon?

How much stability do you need from debt mutual funds as a buffer?

Are you adding international or factor funds because they genuinely fit, or just because they are trending?

Section 3

Direct vs regular mutual funds: cost, control and responsibility

Aspect | Direct mutual funds | Regular mutual funds |

|---|---|---|

Expense ratio | Lower — no distributor commission embedded | Higher — includes distributor commission |

Who guides you | You, or a SEBI-registered advisor you hire separately | Distributor or relationship manager |

Control | Higher control, requires higher analytical skill | Less control, more hand-holding available |

When you choose direct mutual funds, you effectively become your own portfolio manager. You must learn mutual funds deeply enough to handle selection, rebalancing, and risk analysis yourself — or with the help of a SEBI-registered investment advisor.

Section 4

How professionals evaluate a mutual fund: beyond past returns

Most investors look at 1-year or 3-year returns and star ratings. Professional portfolio managers go much deeper. They use a structured fund selection process that combines quantitative and qualitative checks.

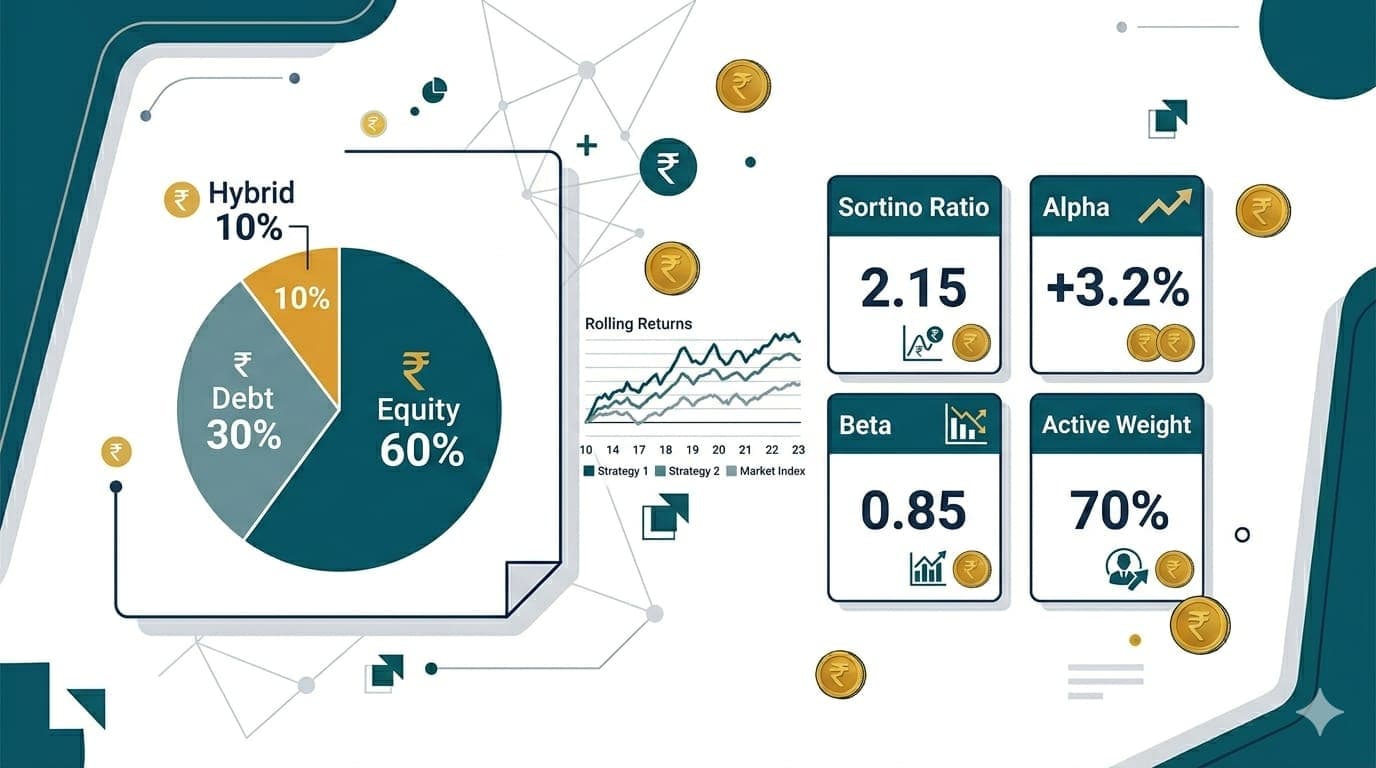

Rolling returns

Check consistency across many periods — not just one lucky phase that happens to align with the review date

Sortino ratio

Measures how much downside risk was taken for the returns delivered — focuses on the volatility that actually hurts you

Alpha and beta

Alpha = manager skill over benchmark after risk adjustment. Beta = sensitivity to market moves. Together they reveal real value-add.

Portfolio analysis

Turnover, concentration, sector exposure — checks whether the strategy matches your comfort with risk and volatility

Did you know

In 2024, US passive mutual funds and ETFs surpassed active funds in total assets for the first time — as more investors shifted toward cost-efficient, rules-based strategies that avoid active management fees in efficient markets.

Section 5

Mutual fund risk analysis: measures every serious investor should know

Risk is not just "high" or "low." Professional risk management involves measuring and comparing risk — so you know what you are accepting before you invest. Mutual fund risk analysis helps you avoid funds that look good on returns but expose you to uncomfortable drawdowns when markets turn.

Standard deviation: How volatile a fund's returns are around its average

Sortino ratio: Downside volatility specifically — matters more for emotional comfort during corrections

Maximum drawdown: The worst historical peak-to-trough fall — helps you test whether you could actually hold through something similar

Beta: How sensitive the fund is to market swings relative to its benchmark

Risk metrics describe the past and cannot predict the future perfectly. They are tools to support judgement — not to replace it.

Section 6

Risk-adjusted returns: why Sortino, alpha and rolling returns matter

Two funds can deliver the same raw return, but one may have done it with much higher volatility. The second fund has better risk-adjusted returns — and is likely to be a more sustainable choice for long-term compounding without behavioural disruption.

Rolling returns, Sortino ratio, and alpha together answer three critical questions: how smooth the journey was, how consistent the returns were across different market phases, and whether the fund manager added value over the benchmark after accounting for risk.

Compare rolling 3-year or 5-year returns against benchmark and category peers — not just point-to-point CAGR

Look for funds with reasonably high Sortino ratio instead of just highest raw returns

Check alpha over meaningful multi-year periods — not just recent short-term rallies

Did you know

Asset-weighted average expense ratios for US mutual funds fell to 0.34% in 2024, saving investors an estimated $5.9 billion in fees — highlighting how cost control directly and measurably supports long-term portfolio outcomes.

Section 7

Portfolio-level analysis: active weights and overlap across your funds

Even if each fund looks good individually, your combined portfolio may be heavily concentrated in the same stocks or sectors — especially if you own multiple funds from the same category without checking overlap.

Active weight calculations measure how your portfolio differs from its composite benchmark and where you are unintentionally taking concentrated bets. This is how professional portfolio managers check for hidden concentration risk.

Which sectors or stocks are overweight or underweight compared to your intended benchmark exposure?

Where are multiple funds giving you effectively the same exposure — reducing true diversification?

Is your portfolio genuinely diversified or just crowded in a few popular themes?

If your portfolio is heavily overweight in the same large caps across several funds, a single market event can hurt much more than expected — even if you "own many schemes."

Section 8

SIP investment strategies: turning monthly contributions into a coherent plan

SIPs are powerful because they build discipline. But most investors start SIPs randomly — based on what a friend or salesperson suggests, without any goal or risk alignment behind the choice.

1

Define the goal and its time horizon before starting any SIP

2

Select the category and risk level first — then choose the specific scheme

3

Review SIP performance and asset allocation annually — not monthly in reaction to short-term results

4

Avoid starting new SIPs in similar funds just because existing ones look "slow" over a short period

Section 9

Learning from institutional practice: Goldman Sachs-style discipline for individuals

At institutions like Goldman Sachs, portfolio managers track performance, risk, and compliance daily — every decision backed by data and documented rationale. The goal is not to turn you into an institutional fund manager, but to bring some of that discipline to your personal portfolio.

Structured review cycles — not impulsive decisions triggered by market headlines or social media

Use of rolling returns, alpha, beta, and active weights — even in a simplified retail-friendly form

Clear documentation of why you added or exited a fund — so you avoid repeating the same mistakes in the next market cycle

Institutional-grade thinking is not about complexity. It is about consistency and accountability in how you run your mutual fund investment decisions — year after year.

Section 10

How a live mutual fund workshop accelerates your learning curve

Scattered videos and articles leave big gaps. A structured, live mutual fund workshop gives you real-time Q&A, portfolio analysis on actual case studies, and guided practice on techniques like rolling returns and Sortino ratio — led by someone with ₹65B+ AUM institutional experience.

What a high-quality workshop should include

Basics for beginners and advanced concepts — rolling returns, Sortino ratio, alpha/beta, active weights — for more experienced investors

Portfolio-level analysis, not just single-fund reviews

SEBI guidelines discussion — so you understand the boundary between educational content and regulated advice

Transparent disclaimers, a money-back guarantee for dissatisfied participants, and time-bound bonus materials

Section 11

Compliance, SEBI guidelines and knowing when to seek professional help

In India, only SEBI-registered investment advisors are allowed to provide personalised, compensated investment advice tailored to your specific situation. Everything in a financial education context — frameworks, skill-building, analytical techniques — is for your own learning and decision-support, not a substitute for regulated advice.

Use workshops and courses to learn mutual fund analysis and portfolio concepts

Use this knowledge to have better, more specific conversations with your advisor

Rely on your SEBI-registered RIA for recommendations that consider your taxes, cash flows, and personal constraints

Education gives you the power to ask the right questions. Regulation ensures that when you do seek personalised advice, it comes from someone accountable under SEBI's framework.

Conclusion

From product buyer to process-driven investor

Building a mutual fund portfolio that genuinely supports financial freedom is not about chasing the newest scheme or reacting to market headlines. It is about clear asset allocation, disciplined SIP investment strategies, and a repeatable process for portfolio analysis that covers risk, returns, and costs together.

As you deepen your financial education, focus on practical skills — rolling returns, Sortino ratio, alpha and beta, and active weight calculations. Combine this with respect for SEBI guidelines and, when needed, guidance from a SEBI-registered advisor. Over time, these habits turn you from a product buyer into a confident, process-driven investor who manages their portfolio with the same seriousness that professionals bring to institutional portfolios.

enjoyed this article?

explore more insights on building wealth.