Mutual fund calculator: the simple tool that can change how you invest forever

Most investors guess their SIP amounts and expected returns instead of running the numbers. Learn how to use a mutual fund calculator properly — paired with rolling returns, Sortino ratio & risk analysis — to build goal-linked investment strategies that actually work.

Mutual fund calculator: the simple tool that can change how you invest forever

Mutual fund education

Around 53.7% of U.S. households owned mutual funds in 2024, and total global mutual fund assets crossed $31.30 trillion in November 2025. Yet most investors still guess their returns, SIP amounts, and risks instead of running the numbers. A mutual fund calculator helps you stop guessing and start making data-backed decisions.

Key takeaways

At a glance

Question | Answer |

|---|---|

What is a mutual fund calculator? | An online tool that estimates future value of your investment or SIP based on amount, duration, and expected return. It supports better planning — not prediction. |

Does it replace professional advice? | No. A calculator is for education and planning. For personalised advice under SEBI rules, consult a SEBI-registered RIA. |

How does it help with financial freedom goals? | It shows, in numbers, exactly what it takes to reach retirement or a corpus target — and reveals how starting earlier or choosing direct plans changes outcomes significantly. |

Can it teach me mutual funds properly? | On its own, no. Used inside a structured workshop, it becomes a powerful learning lab for testing rolling returns, alpha, beta, and SIP strategies. |

Section 1

What a mutual fund calculator really does (and what it cannot do)

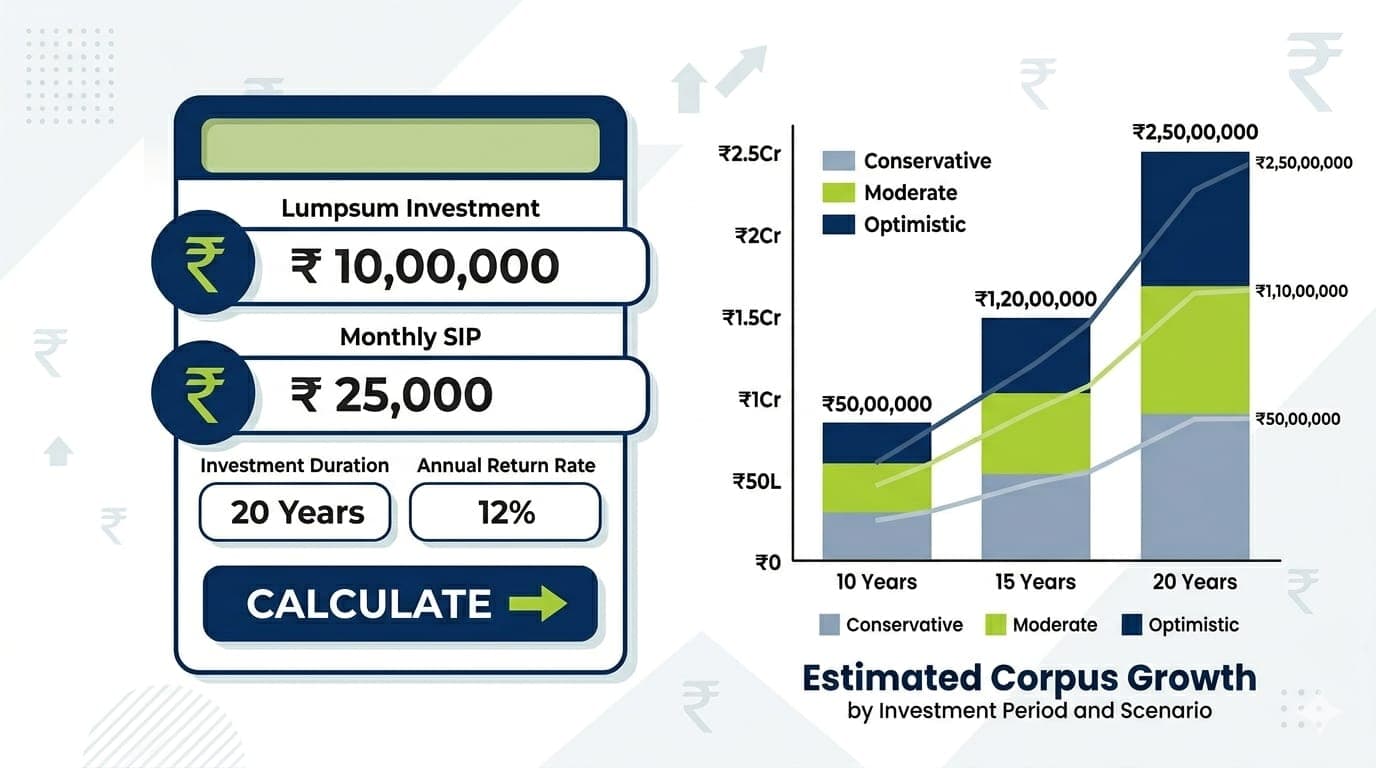

A mutual fund calculator is a simple front-end for compound interest math. You input investment amount, time period, and expected return — and it shows an estimated future value. For SIP investment, you specify a monthly amount and the calculator spreads contributions across the period.

Used correctly, it connects your goals with realistic numbers. Used blindly, it misleads — if you assume projected returns are guaranteed or ignore risk entirely. Calculators are educational aids, not a promise of performance.

Section 2

Types of mutual fund calculators you should know

Lumpsum return calculator

Estimates how a one-time investment grows at a constant rate. Useful for comparing short vs long horizon goals and visualising the impact of starting early.

SIP investment calculator

Models monthly contributions. Shows total invested, total value, and estimated gains — essential for designing realistic SIP strategies around your cash flows.

Goal-based calculator

Works backward from a target corpus to tell you how much to invest monthly. Best for retirement, education, or financial freedom planning.

Cost comparison calculator

Compares direct vs regular mutual fund outcomes by adjusting effective returns for different expense ratios over long periods.

Section 3

Core inputs in any mutual fund calculator (and how to set them)

Most calculators look simple, but your assumptions matter more than the interface. Spend more time on inputs than on the output chart — that is where real financial education happens.

Investment amount: Lumpsum or monthly SIP — match to your actual cash flow

Time horizon: In years or months, clearly aligned with your goal deadline

Expected annual return: Should reflect fund category and realistic historical ranges, not best-case scenarios

Expense ratio or cost: Especially important when comparing direct vs regular mutual funds

Tax assumptions: If the calculator allows it, factor in LTCG/STCG implications

Always build three scenarios — conservative, moderate, and optimistic return assumptions. This reduces disappointment if markets behave differently from your first estimate.

Did you know

In November 2025, total net assets of mutual funds globally reached about $31.30 trillion — meaning even small improvements in your calculator assumptions can have a significant absolute impact on long-term outcomes.

Section 4

Using calculators for SIP investment strategies that fit your life

SIP investing is where calculators become especially powerful. Instead of wondering "Is ₹5,000 per month enough?", you can run multiple simulations across different tenures and return ranges — turning vague goals into concrete monthly commitments.

1

Start from the goal amount and deadline — not from a random SIP figure

2

Work backward using a SIP calculator to find the required monthly contribution

3

Stress-test results by lowering expected returns to see if you are still comfortable

4

Repeat for different fund categories to see how risk affects required SIP amounts

Section 5

Beyond returns: risk-adjusted thinking alongside calculator outputs

Most basic calculators show only the end value. Professional investors always evaluate risk along with return. The goal is to think more like that — even as a retail investor.

Tool | What it adds beyond the calculator |

|---|---|

Rolling returns | Checks return consistency across overlapping periods — not just a single lucky window |

Sortino ratio | Shows how much downside volatility you take per unit of return — focuses on the bad swings |

Alpha and beta | Alpha = outperformance over benchmark; beta = sensitivity to market moves |

Max drawdown | Worst historical fall — helps you mentally prepare for what the calculator's CAGR path can hide |

Section 6

Mutual fund portfolio analysis with calculator-driven scenarios

A calculator becomes far more powerful when connected to portfolio analysis. Instead of testing one fund at a time, you model how different combinations of funds behave together — moving from "fund picking" to real portfolio thinking.

Diversification across equity, debt, and hybrid categories

Weighting of each fund and its impact on risk and projected return

Overlap between funds that might reduce true diversification

Rebalancing frequency and its compound effect on long-term outcomes

Small changes in allocation can produce meaningfully different projected values over 15 to 20 years — which is why asset allocation and fund selection matter far more than trying to guess next year's winner.

Did you know

The FINRA Fund Analyzer covers over 18,000 mutual funds, ETFs, and ETNs — showing how powerful calculator-style tools can be when you want to compare costs and projected values across many options at once.

Section 7

Mutual fund risk analysis: using calculators without ignoring volatility

A calculator can make any fund look attractive if you plug in a high return number. This is where risk analysis is essential — you need to understand how bumpy the ride can be, not just the destination.

Look at maximum drawdowns alongside CAGR — not CAGR alone

Compare beta to see how sensitive your fund is to market corrections

Check the Sortino ratio for downside-focused risk-adjusted returns

Review the SEBI risk-o-meter category for each fund before plugging returns into a calculator

Section 8

Direct vs regular mutual funds: cost calculators and active weight thinking

One of the most practical uses of a mutual fund calculator is comparing direct vs regular plans. Even a 0.5% to 1% difference in expense ratio produces a strikingly large corpus gap over 15 to 20 years of SIP contributions.

How to run a direct vs regular comparison

Keep investment amount, tenure, and expected gross return identical in both scenarios

Input different effective returns that reflect direct and regular expense ratios

Compare end values and total "invisible cost" paid through lower compounding

Active weight calculations add another layer: if a fund claims to be "active" but its active weights are minimal, its NAV hugs the index — which raises questions about whether the higher fee in a regular plan is justified at all.

Section 9

How the live mutual fund workshop turns calculators into a learning lab

A standalone calculator leaves many investors unsure a

enjoyed this article?

explore more insights on building wealth.