Large cap mutual funds explained: smart strategies, real risks, and how to analyse them like a pro

65% of active large cap funds underperformed the S&P 500 in 2024. Yet most investors still pick them by brand name and recent returns. Learn how to analyse large cap mutual funds professionally using rolling returns, Sortino ratio, active weights, and cost analysis.

In 2024, 65% of U.S. active large-cap mutual funds underperformed the S&P 500 index — even before accounting for costs. Over the last 10 years, only about 7% of U.S. large-cap active funds survived and beat their average passive benchmark. Numbers like this should not scare you away — they should motivate you to learn how to analyse funds properly and ask better questions.

Key takeaways

At a glance

Question | Key insight |

|---|---|

What are large cap mutual funds? | Funds that invest in the largest, most established companies — often used as the "core" building block of a mutual fund investment portfolio. |

Are they safe for beginners? | Generally less volatile than mid/small caps, but still carry market risk. Labels alone are not enough — combine with proper risk analysis. |

Active vs passive for large caps? | With most active large cap funds underperforming their benchmarks over time, costs and risk-adjusted returns matter enormously in this category. |

Direct vs regular plans? | Direct plans have lower expense ratios. In large caps where alpha is scarce, cost is often one of the most reliable predictors of long-run outcomes. |

Is this investment advice? | No. Financial education only. For personalised recommendations, always consult a SEBI-registered RIA. |

Section 1

What are large cap mutual funds and why do they matter?

Large cap mutual funds invest predominantly in companies with the highest market capitalisation — typically the top 100 companies as defined by SEBI. These are blue-chip businesses with established models, strong balance sheets, and consistent track records.

For many investors, large cap funds form the "core" of their mutual fund investment portfolio — offering relatively smoother return patterns than smaller companies, better liquidity, and stricter regulatory scrutiny. Combined with disciplined SIP investment and proper risk analysis, they can support long-term goals like retirement, education, and financial freedom. However, choosing a "big name" fund or chasing past performance is not enough — you need skills, not shortcuts, to differentiate genuinely robust funds from those riding temporary trends.

Section 2

Types of large cap mutual funds: active, passive, direct, and regular

Active large cap funds

Aim to beat a benchmark by selecting stocks actively

Higher expense ratios — cost of research and management

Majority underperform passive peers over long periods

Passive large cap funds

Track an index like Nifty 50 or Nifty 100

Low cost — no active stock selection overhead

Performance closely mirrors the benchmark

Direct mutual funds

Bought directly from AMC — no distributor commission

Lower expense ratio by 0.5–1%+

Research and monitoring responsibility is yours

Regular plans

Bought via distributor — commission embedded in expense ratio

Higher annual cost that compounds against you over time

May include distributor guidance (quality varies)

If you are willing to build your own knowledge through financial education, direct plans typically work better in the long run — especially in large caps where even small cost advantages compound into significant corpus differences.

Section 3

Risk and return in large cap funds: what your advisor may not spell out

Large cap funds are often marketed as "safer" or "conservative." While they can be relatively less volatile than mid or small caps, they are still equity funds — exposed to market risk, sector rotations, and valuation cycles. Understanding this upfront prevents disappointment when markets correct.

Core risk metrics you must know

Metric | What it reveals for large cap analysis |

|---|---|

Rolling returns | How the fund behaves over different time windows — not just a single favourable period |

Beta | Sensitivity to the benchmark index — useful for understanding how aggressively the fund moves with the market |

Sortino ratio | Focuses on downside volatility specifically — more relevant than Sharpe for evaluating actual investor experience |

Alpha | Excess return over benchmark after accounting for risk — the ultimate test of active management value |

Active weight | How much the fund deviates from benchmark holdings — low active weight with high fees is a warning sign |

Did you know

Over the last 10 years, only about 7% of U.S. large-cap active funds survived and beat their average passive benchmark — showing how rare genuine, sustained outperformance really is in this category.

Section 4

How to analyse large cap mutual funds like a professional

Most investors look at 1-year or 3-year returns and brand names, then stop. Professionals go several layers deeper. The goal is not to tell you "buy this fund" — but to teach you how to think so you can make independent, repeatable decisions.

1

Define the benchmark — Nifty 50, Nifty 100, or another index that best reflects the fund's stated universe

2

Check consistency of rolling returns across 3-year and 5-year periods vs the benchmark and category peers

3

Evaluate risk-adjusted returns using Sortino ratio and Sharpe ratio — not just raw performance

4

Look at alpha and beta to understand how much return is genuine skill versus simple market exposure

5

Do portfolio analysis — sector weights, top holdings, concentration risks, and active weights vs benchmark

6

Assess expenses and turnover ratio — understand the cost difference between direct and regular plans

Once you run this checklist, many popular large cap mutual funds look very different from what marketing material suggests.

Section 5

Cost, direct plans, and risk-adjusted returns in large cap funds

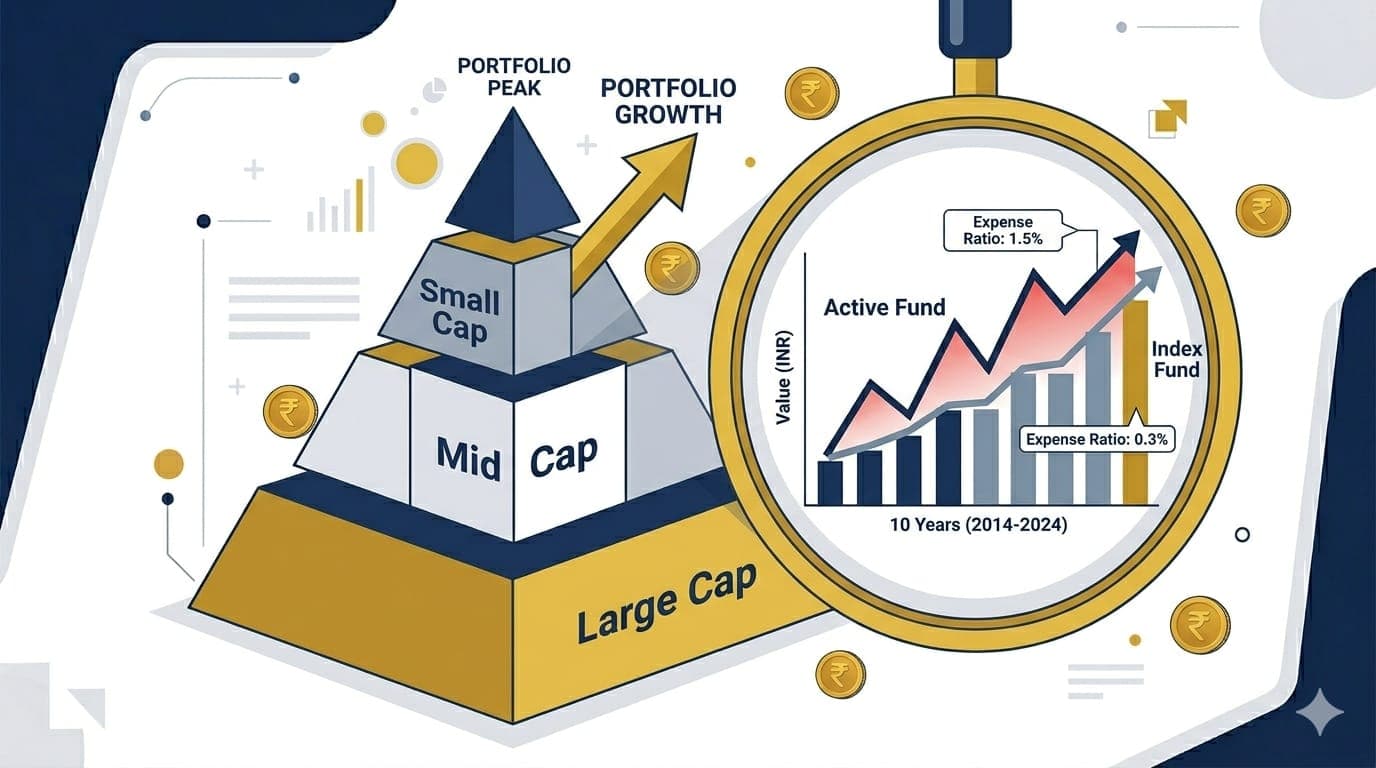

In large caps where many funds closely hug their benchmark, costs are often the difference between beating and lagging the index. The asset-weighted average expense ratio across U.S. mutual funds and ETFs fell to about 0.34% in 2024 — low-cost investing is not a trend, it is a structural shift.

Lower expenses directly lift net returns when gross performance is similar across funds

In categories where alpha is scarce, cost becomes one of the most reliable long-term predictors

Always evaluate Sortino ratio or Sharpe ratioafter feesfor a realistic picture of what you are actually receiving

Ask a simple question about every active fund: "Is the extra fee justified by persistent, risk-adjusted outperformance — or by something a low-cost index fund could replicate?"

Did you know

Among large-cap funds, the cheapest funds outperformed their passive peers over 10 years in about 13% of cases — compared with roughly 1.3% for the most expensive funds. Cost is strongly linked to long-run outcomes in this category.

Section 6

Large cap mutual funds and SIP investment strategies for different life goals

Goal type

Typical horizon

Role of large cap funds

Retirement planning

15+ years

Core equity allocation with SIPs and periodic portfolio analysis

Children's education

8–15 years

Blend of large cap and other categories, with gradual derisking as the goal nears

Long-term wealth creation

10+ years

Stable engine focused on quality, cost efficiency, and risk-adjusted returns

Shorter goals (car, vacation)

3–5 years

Limited or no pure equity allocation depending on risk profile

These are general frameworks — not recommendations. A SEBI-registered RIA should validate your final asset allocation based on your specific circumstances.

Reviewing SIPs with portfolio analysis

Setting up a SIP is not the end of the story. An annual or semi-annual portfolio review should check whether the fund still adheres to its large cap mandate and style, how its rolling returns and risk metrics compare with peers, and whether any life changes require rebalancing.

Section 7

Learning from institutional-grade research: Goldman Sachs-style thinking for retail investors

The workshop curriculum is guided by an instructor with ₹65,000 crore+ AUM experience and training in research-driven environments including Goldman Sachs strategies. Those methods are adapted for everyday investors — without overwhelming jargon, but with the same analytical discipline.

Focus on data, not stories or headlines

Use consistent factor-based and risk-based frameworks to evaluate funds

Separate skill from luck using rolling returns and alpha analysis

Understand regime changes — where certain styles or sectors temporarily dominate and why

The live, interactive workshop format means you can ask questions in real time about large cap fund factsheets and portfolios, work through live risk analysis examples, and see institutional frameworks applied step by step — not in a one-way lecture.

Section 8

Skills you actually learn in the mutual fund workshop

Many educational programs talk in high-level concepts then leave you with generic advice. The goal here is specific: walk away confident that you can independently evaluate a large cap fund using public data and a repeatable process.

How to read and interpret a large cap fund factsheet and scheme document

How to calculate and interpret rolling returns for different time periods

How to use Sortino ratio, alpha, and beta for risk-adjusted comparison between funds

How to perform portfolio analysis — sector allocation, factor exposures, and concentration checks

How to compute basic active weight and interpret a manager's true conviction vs benchmark hugging

A money-back guarantee is included if you attend the live sessions and still feel you did not gain meaningful clarity on large cap analysis. Limited-time bonus materials — analysis templates, checklists, recorded Q&A replays — are available for specific batches.

Section 9

Compliance, SEBI guidelines, and the role of advisors

All content is educational — not advisory. No specific buy or sell recommendations are made on any large cap mutual funds or securities. The goal is to help you interpret information already available through SEBI-mandated disclosures and fund house documents.

Large cap mutual funds carry market risk. Past performance, ratios, and portfolio data are analytical tools — not guarantees. Structured financial education reduces avoidable mistakes and gives you a clearer picture of what you own and why, but it cannot eliminate uncertainty.

Even with strong analytical skills, portfolio construction and financial planning depend on your unique situation. Only a SEBI-registered investment advisor (RIA) can legally provide personalised advice on which funds to invest in, in what proportion, and for how long.

Section 10

Building a long-term large cap strategy: putting it all together

1

Clarify goals and horizons for which large cap funds will be used

2

Shortlist funds that fit SEBI-defined large cap category with transparent disclosures

3

Run fund selection checks — rolling returns, risk-adjusted returns, portfolio characteristics

4

Decide on SIP strategies aligned with your cash flows and risk tolerance

5

Choose between direct vs regular plans — keeping cost impact clearly in mind

6

Review annually with portfolio analysis and risk metrics — ideally in consultation with a SEBI-registered RIA

Conclusion

Apparent simplicity hides real complexity — build the skill to see both

Large cap mutual funds remain a central building block for many investors, but their apparent simplicity can be misleading. With a majority of active large-cap funds failing to beat benchmarks over time, relying on brand names or raw past returns is no longer enough.

By learning to use rolling returns, Sortino ratio, alpha, beta, and active weight calculations — and understanding the trade-offs between direct and regular plans — you put yourself in a stronger position to pursue financial freedom responsibly. Financial education reduces avoidable mistakes. Professional advisory ensures personalised application. You need both.

enjoyed this article?

explore more insights on building wealth.