Expense ratio in mutual funds: the simple cost that quietly eats into your returns

The expense ratio quietly reduces your mutual fund returns every single year — yet most investors ignore it. Learn what it includes, how it compounds over 20 years of SIPs, why direct plans beat regular plans on cost, and when a higher expense ratio can actually be justified.

Expense ratio in mutual funds: the simple cost that quietly eats into your returns

|Mutual fund education

Most investors focus on past returns and star ratings — but ignore the one number that affects their mutual fund investment every single year: the expense ratio. In 2024, the asset-weighted average expense ratio for all U.S. mutual funds and ETFs was just 0.34%, yet investors still paid billions in fees that directly reduced their wealth.

Active equity funds (U.S., 2024)

0.60%

Asset-weighted average expense ratio for actively managed funds

Passive index ETFs (U.S., 2024)

0.11%

Asset-weighted average — nearly 6x cheaper than active management

Key takeaways

At a glance

Question | Answer |

|---|---|

What is an expense ratio? | The annual percentage fee a mutual fund charges to manage your money. It is deducted from the fund's assets daily and reduces your returns automatically every year. |

Why does a small difference matter? | Even 0.5% higher costs, compounded over 15–20 years of SIP investment, can reduce your final corpus by several lakhs. Cost control is a core part of smart fund selection. |

Direct vs regular — how do expense ratios differ? | Direct mutual funds exclude distributor commissions, so their expense ratio is lower. Regular plans include commission, making them more expensive for the same underlying portfolio. |

Can a higher expense ratio ever be justified? | Yes — but only if the fund consistently delivers better risk-adjusted returns (alpha, Sortino ratio, downside protection) after accounting for the extra cost. |

Is this investment advice? | No. Education only. For personalised recommendations, consult a SEBI-registered RIA. |

Section 1

What is expense ratio and why it matters more than you think

The expense ratio is the annual fee a mutual fund charges to manage your money, expressed as a percentage of the fund's average assets. It covers management fees, administration, record-keeping, marketing, and other operating costs.

You never pay this fee separately — the fund deducts it from the portfolio daily, which quietly reduces your returns. For someone running SIPs for 20 years, this small percentage difference can create a significant gap in final wealth, even if two funds show similar past performance. Think of it as annual "rent" you pay for using the fund. If the rent is high, the quality of service must clearly justify it.

Section 2

Components of expense ratio: what exactly are you paying for?

An expense ratio of 1.5% or 0.3% is not a single fee — it is a combination of multiple cost heads. Understanding these components helps you evaluate whether you are paying fairly for the value you receive.

Fund management fee: Compensation for the fund manager and research team who make buy/sell decisions.

Administrative and operational costs: Custody, accounting, record-keeping, legal, and audit costs.

Marketing and distribution expenses: In regular plans, this includes distributor commissions and promotional costs.

Registrar and transfer agent (RTA) fees: Costs related to handling investor records and transactions.

In direct mutual funds, the distribution and commission component is largely absent — which is why the expense ratio is typically lower compared to regular plans of the same scheme.

Section 3

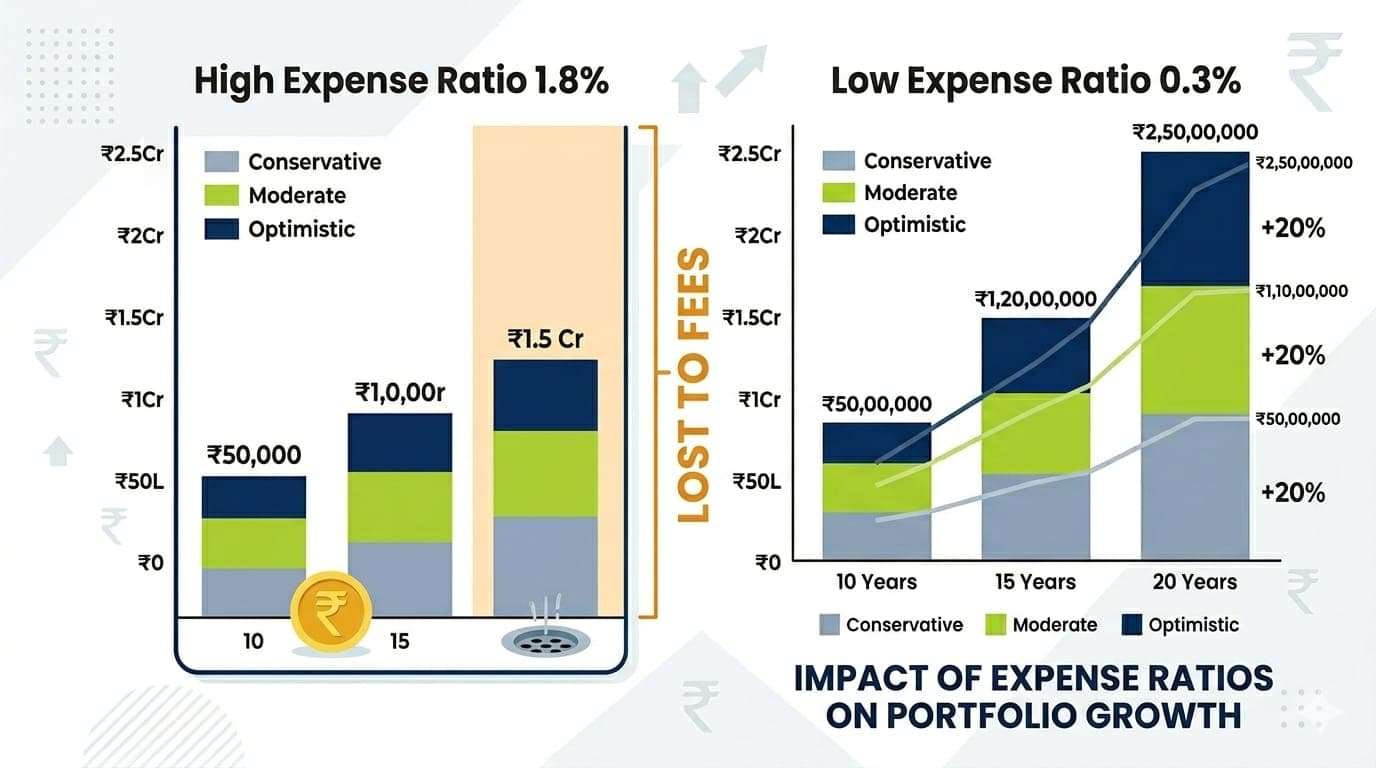

How expense ratio affects SIP investment and long-term wealth

For long-term investors running monthly SIPs, the expense ratio is one of the most important levers of wealth creation. Even if you cannot control market returns, you can control your costs.

Assume two equity funds with identical portfolios and gross returns — one at 1.8% expense ratio, the other at 0.8%. Over 15 to 20 years of SIP investment, the lower-cost fund typically delivers a significantly higher final corpus, simply because less is deducted each year and more stays in the compounding base.

High expense ratios drag down compounding year after year — silently, without a separate bill

Low-cost funds allow more of the market return to stay in your portfolio

Expense ratio should be a core screening criterion alongside risk and consistency

Did you know

The asset-weighted average expense ratio for all U.S. mutual funds and ETFs fell to 0.34% in 2024, down from 0.36% in 2023 — saving investors about $5.9 billion in fund expenses in a single year.

Section 4

Expense ratio in mutual fund selection: a practical framework

Expense ratio is not the only factor in fund selection — but it is a powerful early filter. Cost should be one of the first checkpoints, followed by quality, risk, and consistency.

1

Define your goal and horizon — retirement, education, wealth building

2

Pick the right category — large cap, flexi cap, short duration debt, etc.

3

Screen for competitive expense ratios within that category, especially for efficient segments like large caps and index funds

4

Evaluate risk-adjusted returns using alpha, beta, and Sortino ratio

5

Check consistency with rolling returns, not just point-to-point CAGR

Expense ratio should rarely be the only reason to select or exit a fund. See it as one part of a comprehensive portfolio analysis that considers both cost and performance quality.

Section 5

Direct vs regular mutual funds: expense ratio and investor control

The core scheme portfolio of direct and regular plans is usually identical — but expense ratios differ because of how the product is distributed.

Aspect | Direct plan | Regular plan |

|---|---|---|

Distribution/commission | Not included | Included in expense ratio |

Typical expense ratio | Lower | Higher |

Who is it for | Investors comfortable making decisions themselves or guided by a fee-only SEBI RIA | Investors who rely on distributor relationship for execution and guidance |

Financial education needed | Higher — you take more responsibility for decisions | Still important, but many investors rely on their distributor |

Section 6

Expense ratios, active vs passive funds, and risk-adjusted returns

If index funds are so cheap, why do people still invest in higher-cost active funds? The answer lies in the trade-off between cost and potential outperformance.

Passive funds (index mutual funds, index ETFs) have very low expense ratios — averaging 0.11% in 2024 — because they simply track a benchmark.

Active funds charge higher expense ratios to pay for research teams and stock selection, targeting alpha — outperformance over the benchmark.

Whether the extra cost is justified depends entirely on the fund's long-term risk-adjusted returns. Instead of asking "Is this fund cheap?", ask: "Is this fund giving me better performance for each unit of risk and each rupee of cost?"

Metric | What it reveals about cost justification |

|---|---|

Alpha | Excess return over benchmark after adjusting for risk — the core test for active fee justification |

Beta | Market sensitivity — high beta with high cost is often a poor combination |

Sortino ratio | Return per unit of downside risk — shows if you're being paid for volatility you take on |

Rolling returns | Consistency check — a fund should justify its fees across multiple market cycles |

Did you know

In 2024, asset-weighted expense ratios for active U.S. equity funds were about 0.60%, while passive funds averaged only 0.11% — investors paid roughly 5x more for active management on average.

Section 7

How we teach expense ratio analysis in the mutual fund workshop

Many investors tell us: "Nobody explained expense ratio to me this clearly." That gap in financial education is exactly what the live, interactive workshop addresses — building skill, not selling products.

The lead instructor brings Goldman Sachs strategies and fund management experience, having worked with portfolios exceeding ₹65,000 crore in AUM. Institutional portfolio analysis frameworks are simplified into practical, easy-to-apply tools.

What you learn about expense ratios specifically

How expense ratios are calculated and debited daily — not as a one-time charge

Where to find this number in mutual fund documents, fact sheets, and apps

How to compare expense ratios across categories and fund houses meaningfully

When a higher expense ratio might be acceptable based on long-term performance data

Section 8

Advanced techniques: linking expense ratio with portfolio analysis

As you progress in financial education, you move from analysing one fund at a time to evaluating your entire portfolio. Expense ratio then becomes a portfolio-level metric — not just a scheme-level number.

Weighted average portfolio expense ratio

For each fund: multiply its expense ratio by its weight in your portfolio. Sum all results to get your true annual cost across the entire portfolio.

Active weight and fee justification

If an actively managed fund closely mirrors its benchmark holdings but still charges a high expense ratio, you may be overpaying for essentially index-like exposure. Active weight analysis measures how different your fund actually is from the index — and helps you judge whether the premium fee is genuinely earned.

Section 9

Expense ratio, mutual fund risk analysis, and SEBI guidelines

Expense ratios in India are subject to SEBI guidelines, including category-wise caps and slab structures based on AUM. Key protections for investors include:

SEBI sets maximum Total Expense Ratio (TER) limits for different categories and AUM sizes

Fund houses must disclose TER regularly and inform investors about any changes

Specific rules govern how much can be charged for distribution, brokerage, and other expenses

Even within these caps, funds choose where to sit within the permissible range — which is why you still see meaningful variation across similar funds. When analysing risk, also consider cost risk: the risk that excessive fees erode long-term returns even if markets perform well.

High risk + high cost = dangerous combination if performance doesn't compensate

Moderate risk + low cost = often more suitable for core portfolio holdings

Section 10

Money-back guarantee, live learning, and why cost education cannot wait

Most people learn about expense ratios only after investing for years and missing out on potential gains. The goal is to bring cost literacy to the front of your financial education journey — not the back.

The workshop is live and interactive, not a one-way recorded lecture. You can ask questions in real time, clarify doubts about expense ratios and SIP strategies, and see real-world examples from actual fund documents. A money-back guarantee is included if the session does not add clarity or practical skills to your mutual fund decision process.

All content is designed to empower you as an investor — not to replace a SEBI-registered advisor. Think of the workshop as your coach for understanding concepts like expense ratio, while your RIA helps you apply them to your unique situation.

Conclusion

The earlier you understand costs, the more your money compounds

The expense ratio may look like a small percentage — but its impact on long-term wealth is anything but small. For every mutual fund investment you make, this single figure quietly shapes how much of the market's return actually reaches you.

By combining cost awareness with proper mutual fund risk analysis, SIP investment discipline, and structured portfolio analysis, you give yourself a far better chance of achieving financial freedom. The earlier you understand costs, the more years you give your money to grow efficiently.

enjoyed this article?

explore more insights on building wealth.